Power Sustainable Closes CAD$110m Term Loan Investment in telMAX

Power Sustainable Closes CAD$110m Term Loan Investment in telMAX

Power Sustainable secures over US$330M commitments for new middle-market private equity strategy

Potentia Powers Up: Acquiring Repowered 240 MW Big Sky Wind Project

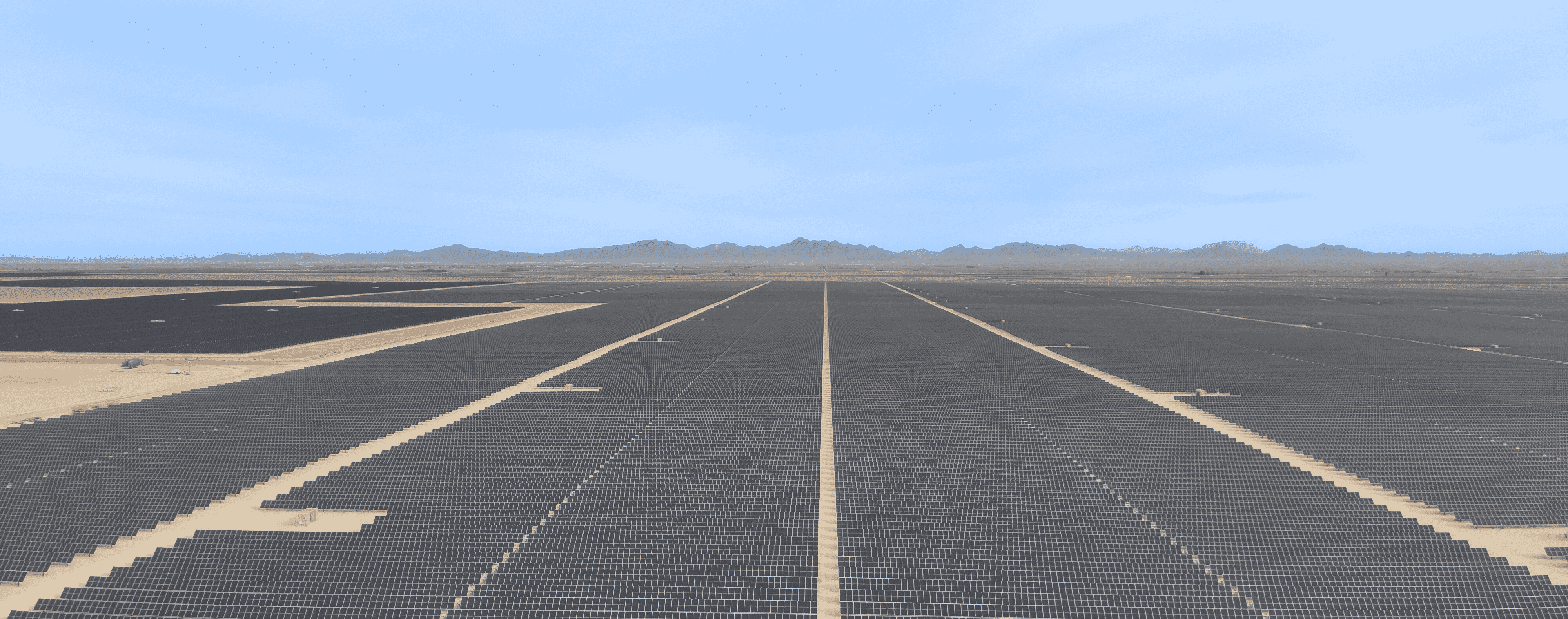

EDF Renewables North America and Power Sustainable Energy Infrastructure Announce Commercial Operation of Desert Quartzite

Power Sustainable Closes CAD $85M Term Loan Investment in Canadian Fiber Optics Corporation (“CFOC”)

Power Sustainable’s Food Private Equity Strategy Delivers on Fundraising, Capital Deployment, and Value Creation Objectives in 2024

Power Sustainable Appoints Delia Cristea as Chief Operating Officer

Power Sustainable Appoints Bruce Heyman as CEO to Lead Expansion

Power Sustainable announces new appointment to Board of Directors

Power Sustainable invests in EDF Renewables North America solar and storage project

Makers of kitchen recycling machines imagine a new, less gross way to dispose of food waste

Food Cycle Science Secures Strategic Investment from Power Sustainable Lios to Accelerate Growth

Centers of Attention: The case for digital infrastructure credit

Power Corp.’s sustainable-investing arm gains familiar new shareholder